Dear Clients and Friends,

The financial media is full of articles and reports about the challenges of investing in China. Many investors wonder if China is even investible given the current challenges its economy faces and the geopolitical tensions surrounding Taiwan, and potential western sanctions; the list goes on.

While we will share some observations about how we navigate this major market on behalf of our clients, it’s important to understand that our research-focused, bottom-up investment approach is driven by company fundamental analysis as opposed to macroeconomic prognostications. Nevertheless, we are very aware of the significant macro issues and pay attention to them as we evaluate investment candidates in China. Therefore, while we do the work to look at investing in companies in China, this does not mean that we are necessarily bullish about China. As with all investments that we make, we do our fundamental work to determine if our estimation of the risk/reward trade-off (relative to opportunities elsewhere) is appropriate for deployment of client capital.

To provide a bit of historical perspective, when Charles Brandes founded the firm in 1974, his first client asked him if value investing principles could be applied outside of the United States. Recall that Graham & Dodd’s seminal work, Security Analysis, confined itself almost entirely to U.S. securities. In 1974, it was unusual for U.S.-based institutional investors to look overseas. However, since his first client was a non-U.S. investor with investments in Canada and Europe, Charles started off the firm with a global perspective.

For almost 50 years, that global perspective has informed us that despite macro tensions and concerns, attractive investment opportunities can be uncovered if one is prepared to do the fundamental analysis. Over the years, we have noticed that some investors approach investing in countries outside of key developed markets as a simple binary, risk- on or risk-off decision without much consideration of individual company fundamentals. This is particularly true, in our observation, when it comes to companies based in “volatile” emerging markets. However, we don’t subscribe to this binary decision framework and intentionally choose a more nuanced approach where the prudent investor may be able to uncover attractive investment opportunities despite macro concerns.

An October global survey of fund managers by Bank of America found that they believed shorting China equities was second most-crowded trade (only the long big-tech trade was more crowded).1 Is fundamental analysis or a binary macro call driving this short trade? Perhaps Warren Buffett’s lesson on fear and greed—be fearful when others are greedy, and greedy when others are fearful—can help explain why doing fundamental analysis as opposed to making a binary decision makes sense even when there are a lot of concerns and uncertainties. Similarly, being long big-technology stocks at this point in 2023 is certainly a crowded trade and possibly an example of the greed in Buffett’s lesson.

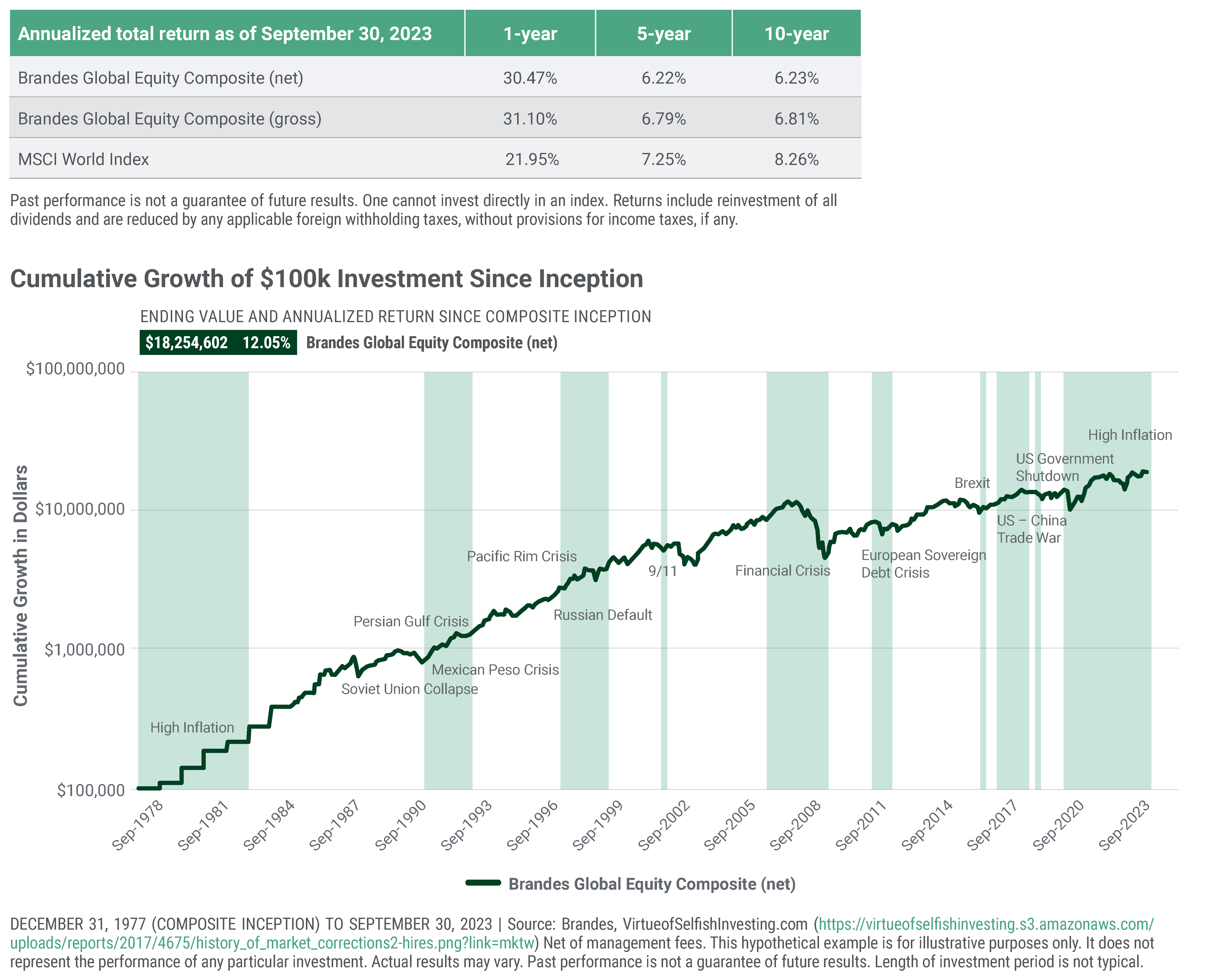

Our nearly 50-year experience investing across global markets tells us that not all heightened macro concerns ultimately come to fruition. For the most- part, developed and emerging countries operate rationally and try to avoid dire consequences from macro and geopolitical actions. However, unexpected geopolitical events can occur, leading to potentially negative outcomes, but we view them as more the exception and not the rule. Based on our experience, periodic global crises happen, but taking measured exposures and holding a diversified portfolio can be justified and rewarding, as exemplified by the long-term performance of our Brandes Global Equity Strategy in the table below.

Given our battle-tested deep experience, it’s not surprising that we don’t subscribe to the binary choice theory when it comes to macro and geopolitical concerns. Indeed, the volatility and uncertainty that macro concerns and geopolitical issues pose, in our opinion, often provide opportunities for investors (especially value investors) who are prepared to do the fundamental analysis, look beyond the immediate issue, and rationally assess whether companies can find their way through the problem du jour.

Keep in mind that when we invest in a company that is operating in a country with lots of macro risks, we typically look for a deeper discount (margin of safety—the discount of a security’s market price to our estimate of its intrinsic value) than we look for with a similar company in a “less risky” country. Those deeper discounts can come about from a variety of reasons including inherent country risks as well as global investors making the binary choice mentioned above.

So, with that background, how are we dealing with the macro and geopolitical issues currently facing China?

When it comes to China, the financial media is replete with reports about slowing GDP (gross domestic product) growth, a growing real estate crisis, youth unemployment, tensions with the west possibly leading to more sanctions, and the prospect of hostilities with Taiwan. We believe our clients expect us to navigate this uncertainty and be prepared to invest if, in our judgement, the risk/reward equation is attractive. Again, we would note that this perspective—that it’s important to continue to consider companies in China—should not be conflated with Brandes being particularly bullish on China. Rather, it is a reflection that we find some Chinese companies that are fundamentally well-positioned and are priced attractively from a risk/reward perspective.

Regular readers of our letters will know that we are organized as teams (investment committees) to manage client portfolios and that we don’t let macroeconomic forecasts be the primary driver of our investment decisions. Rather, we believe that we have to do detailed company-by-company analysis to arrive at an estimate of a company’s intrinsic value, and we attempt to take into account all material issues impacting a company as part of that analysis. In the case of companies operating in China (as well as companies domiciled outside of China that derive significant portions of their revenues from China), we try to consider all the relevant macro issues. The members of the relevant investment committee debate these issues as they relate to a specific company and seek consensus on an estimate of intrinsic value and on a possible allocation within a portfolio.

Investment committees at Brandes can incorporate our assessment of macroeconomic risks in our estimates of intrinsic value through several avenues:

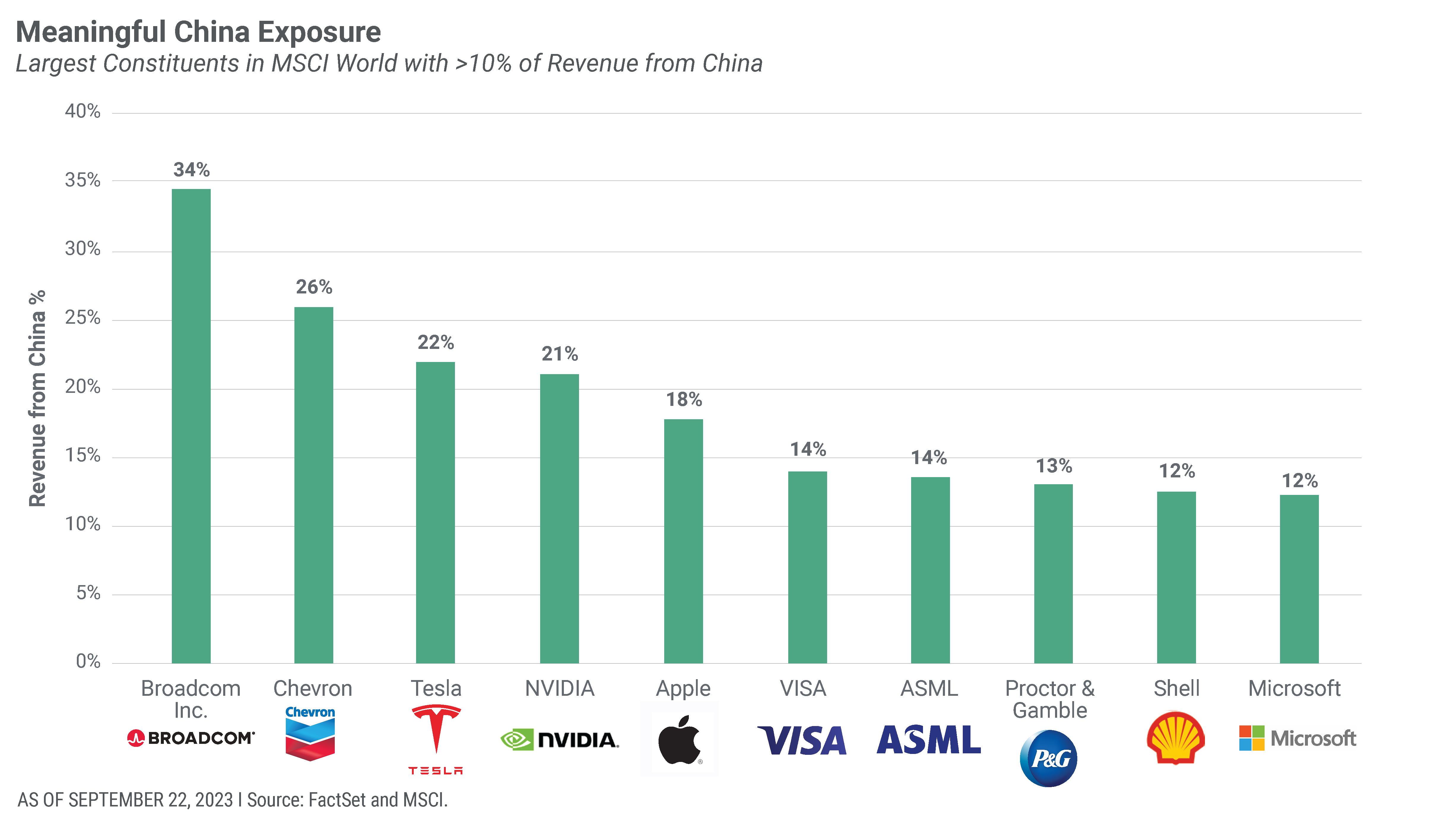

When working through the China conundrum, it’s not only companies domiciled in China that one has to consider. Given China’s role as a primary engine of global economic growth for the past two decades, there are many companies domiciled outside of China that derive a significant proportion of their revenues from China and are subject to secondary effects of China’s policies and geopolitical issues. The table below details significant Chinese exposure for many non-China domiciled companies.

While the nexus to China is different in many cases for these companies compared to companies domiciled in China, they are not immune to China risks. Investors who have taken a binary approach to China (invest or don’t invest) may apply a similar approach to businesses with a high degree of exposure to China. Once again, in our opinion, this “blunt instrument” approach fails to consider company-by-company fundamentals that may mask attractive investment opportunities.

Nevertheless, we acknowledge that it’s very difficult to quantify how China’s geopolitical issues or government actions (their own or those of western governments) will play out. Is this a reason to make a binary decision about investing in a Chinese company? We think not. Real as they are, many of these concerns have more to do with news flow and hype as opposed to fundamental changes for the company we are considering.

We believe it’s in China’s best long-term interests to maintain, as much as possible, the status quo. For instance, China accounts for almost 30% of global manufacturing. China has a very big stake in wanting to maintain its strong global manufacturing position. Acting rationally, China will not want to be sanctioned out of this dominant position.

However, we have no particularly unique insight that says definitively that China will act rationally and in what we believe are its best interests. Indeed, one only needs to look at Russia’s invasion of Ukraine in 2022 for evidence of a state acting in a way that has been detrimental to its economic interests. We argue that this is the exception rather than the rule. While macro and geopolitical challenges are more common than one might think, the markets and the countries involved tend to find a way to rebound from the challenges and the worst-case scenario for investors is not always the outcome.

We acknowledge that the challenges facing China and the resulting potential impacts on global economies are significant. Every investor has their own risk parameters and tolerances. Some investors might decide to forego investing in China altogether and be very satisfied with available opportunities elsewhere. We are not arguing against that. Rather, we are saying that considering the China conundrum is more nuanced than a simple binary decision. The presence of uncertainty, of unknowable factors, and of unquantifiable issues, creates volatility that can potentially present attractive investment opportunities for the prudent value investor.

This was my first trip to China in four years due to the pandemic, and several things stood out to me. First, the advancement in transportation was impressive given the country’s investment in high-speed rail and subway network. Imagine a one-hour trip from Boston to New York, or a 2.5-hour train ride from Los Angeles to San Francisco; the equivalent is reality in China. Second, China’s logistic capabilities have greatly increased, making its e-commerce penetration rate among the highest globally. The same is true for digital infrastructure, especially when it comes to online payment. China has become a near cashless society, with folks using their phones to pay for almost everything, from utility bills to groceries and street vendors. Facial recognition is used everywhere, from company/school college entrances to boarding trains or airplanes. While such widespread usage of facial recognition has boosted artificial intelligence (AI) technologies, it has also evoked concerns about privacy and surveillance.

Another thing that stood out to me was the progress in manufacturing and design. Known as the factory of the world, China has not only substantially improved its manufacturing quality, but also expanded its design capabilities. Lastly, I noticed that attitudes toward the environment have changed significantly. While smog was a regular occurrence decades ago, it was generally greener and cleaner almost everywhere I went this time. It didn’t come without a price, however. I heard firsthand from a company management how the upcoming carbon trading policy has increased prices and would result in the shutdown of its private coal power plants.

Amid all these advancements, it was also clear that the economy is sputtering as two important economic engines, namely residential housing/construction and exports, were both slowing down. Sentiment seemed subdued everywhere I went. Government’s emphasis on ideology and continued crackdown on corruption appeared to have played a significant role in that “lay low” attitude. Despite all these, one start-up that I met (medical diagnosis technology using AI) was going full speed, while almost all other firms I visited were trying to innovate and find the next growth engine. So perhaps, beneath the layer of gloom and doom lay the seeds of advancements for the future.

During our almost 50 years in business, we’ve seen stories like this play out periodically. One of our senior research analysts, Yingbin Chen, was in China in July and August 2023 for nine city stops on the mainland (Guangzhou, Guilin, Wuhan, Beijing, Shanghai, Nanning, Guangzhou, Zhuhai, Shenzhen) and a stop in Hong Kong. She met with several companies that we hold within Brandes portfolios and had the opportunity to assess the investing landscape in person. Observing China’s historical and current behavior, we believe that the country and its companies still represent select investment opportunities. Therefore, when it comes to China right now, we do not see a reason to consider China as completely uninvestible. Rather, we draw on our experience in navigating global markets and allow our fundamental company-by-company analysis to be the primary driver of our investment decisions.

Thank you,

Brandes Investment Partners